Economic Policy Institute, Washington DC

10 August 2005

Can CAFTA save textile and apparel producers?

Some proponents of the Dominican Republic-Central American Free Trade Agreement (CAFTA) believe that it will stimulate apparel industry employment in Central America. According to a University of Michigan study, CAFTA will increase textile and apparel employment in Central America by 283,000 jobs, or 41%. [1] The U.S. Trade Representative’s (USTR) office claimed that, because "garments made in the region will be duty-free and quota-free under the Agreement only if they use U.S. or regional fabric and yarn, thereby supporting U.S. jobs," CAFTA would in turn "provide regional garment-makers-and their U.S. or regional suppliers of fabric and yarn-a critical advantage in competing with Asia." [2]

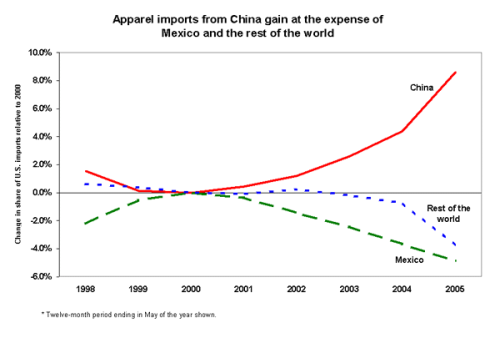

Similar claims were made for the North American Free Trade Agreement (NAFTA), but new data reveal that the U.S.-Mexico textile and apparel complex has been unable to compete with the flood of imports coming into the United States from China. Since 2000, Mexico’s share of U.S. apparel imports has fallen 4.9 percentage points, and total apparel imports from Mexico have declined by $1.5 billion. Imports from Mexico have been displaced by an increase in apparel imports from China. Imports from the rest of the world, as a share of the U.S total, peaked in 2002, shortly after China entered the World Trade Organization (WTO), and their share has fallen by 3.7 percentage points since 2000.

Furthermore, as U.S. apparel imports from Mexico have fallen over the last four years, U.S. exports of fiber, yarn, fabric, and textiles to Mexico have declined 1.4%, or by about $50 million between 2001 and 2005. Thus, it appears that the strategy of using NAFTA to unite the U.S. textile industry with Mexico’s apparel producers has not proven successful in the long run.

China’s share of U.S. apparel imports has increased at an accelerating pace since it entered the WTO in 2001, particularly since the global system of apparel quotas was eliminated on January 1, 2005. Its total share of U.S. imports increased 8.6 percentage points between 2000 and 2005. Given these trends, it is highly unlikely that textile and apparel producers in the CAFTA countries, or the U.S. textile industry, will effectively "Unit[e] to compete with Asia," as the USTR claimed.

Since July 2000, over 500 factories and 90,000 apparel jobs have disappeared in Mexico’s export processing zones. [3] In the same period, the United States has lost 212,000 textile jobs and 305,000 apparel jobs. The notion that 283,000 textile and apparel jobs will be created in Central America as a result of CAFTA is a pipedream. It is based on a model that is driven only by changes in tariff and non-tariff barriers, and it ignores the role played by the enormous surge in China’s exports. Those who believed that this treaty will save U.S. textile jobs or build up these industries in the CAFTA countries will be badly disappointed.

This week’ Snapshot was written by EPI economist Robert E. Scott and research assistant David Ratner.